The Australian Taxation Office (ATO) has recently issued Taxpayer Alert TA 2026/1 targeting property developers which use a development management agreement structure which is commonly used in the property development industry.

The arrangement being targeted is one where a developer has a ‘development management entity which has a contractual arrangement (development management agreement) with a landowner to develop the land.

This is commonly used with a commercial objective to provide asset protection and risk management to separate the risky development activities from the underlying land which is often purchased in a special purpose entity (trust or company).

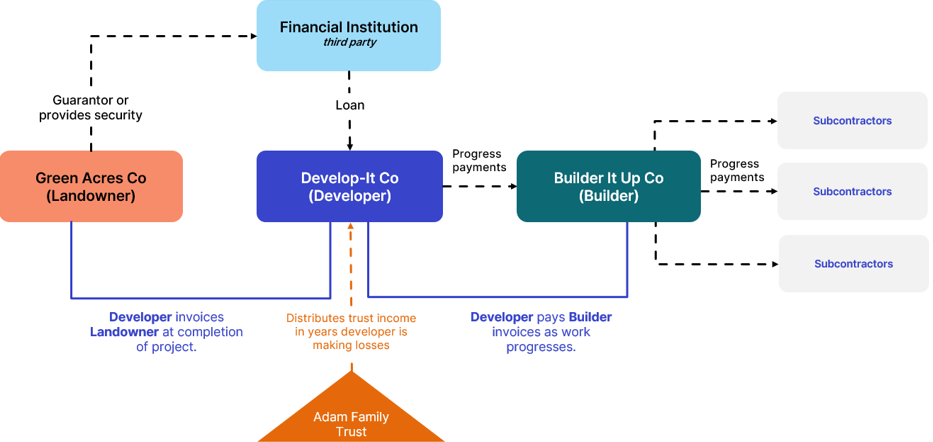

An example of the development structure (from TA 2026/1) which the ATO has outlined its concerns is below:

Diagram 1: Typical long-term construction contract arrangement – exploiting developer’s losses

The ATO’s concern is with developers which control both the land and development management entity and have artificially separated the land and development management to gain a tax advantage.

The ATO highlights particular concerns where a development management entity delays invoicing the landholder to generate losses to offset against other income under the developer’s control.

It is reviewing situations that:

While the use of development management agreements are commercial in nature and claiming of tax deductions for development activities by the development manager are allowed under the tax law, the ATO advises these arrangements may be a scheme under which the general anti-avoidance provisions in Part IVA may apply if there is a dominant purpose of tax avoidance.

The ATO advises it will:

Exant Advisory assists many property developers with tax advice and tax compliance. If you have any concerns with your structure, please contact your usual Exant Advisor, or one of our Partners, Nathanael Lee or Jamie Towers via the form below or on 07 3218 3900.

Author: Jamie Towers, Tax Partner