Claiming to be a budget of resilience and reform, the Government advises it is helping Australians now and building Australia's future by:

In particular, the Federal Budget Tax Brief highlights the Government’s proposed tax reform package which contains 3 key parts and claims it creates:

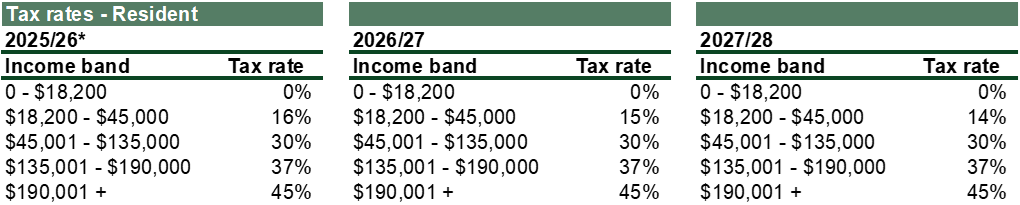

While the 2026-27 Federal Budget focused on broad tax and investment reforms, superannuation remained largely on the sidelines.

The full Budget papers are available at www.budget.gov.au and the Treasury ministers’ media releases are available at ministers.treasury.gov.au.

Exant Advisory's tax and superannuation highlights are set out below.

From 1 July 2027, the 50% capital gains discount (CGT discount) will be replaced with cost base indexation for assets held for more than 12 months, with a 30% minimum tax on net capital gains applying from that date. This will apply to all CGT assets except new homes, including pre-CGT assets, held by individuals, trusts and partnerships.

Cost base indexation

Cost base indexation, which was replaced in September 1999 with the CGT discount, works by adjusting the cost base of the relevant CGT asset. Please refer to our earlier article on how indexation works: What is Capital Gains Indexation and why does it matter?

The measure essentially restores the taxation of CGT assets by applying inflation-adjusted indexation based on the Consumer Price Index (CPI) to tax real gains. Indexation will be calculated using CPI similar to the pre-September 1999 method. The ATO will provide guidance and tools to support taxpayers calculating this adjustment.

Importantly, a minimum tax of 30% will be applicable to realised capital gains accrued from 1 July 2027, after indexation has been applied.

Existing investments

Transitional arrangements will apply to existing investments. Existing assets purchased and sold before 1 July 2027 will still be eligible for the CGT discount. The CGT discount will also continue to apply to gains accrued until 1 July 2027 for assets purchased prior to that date, regardless of when the actual CGT event is triggered. The difference will be calculated by reference to the difference in the asset’s cost base and its value as at 1 July 2027. Indexation and the minimum 30% tax will be used to calculate CGT on gains accruing from 1 July 2027 (using the asset’s value at 1 July 2027 as the asset’s cost base).

Determining an asset's value

An asset’s value at 1 July 2027 will be determined by taxpayers as part of their tax return in the year the asset is realised. Taxpayers can either:

These transitional arrangements also apply to legacy assets, including pre-CGT assets. Capital gains arising on pre-CGT assets before 1 July 2027 will remain exempt from CGT.

Owners of new builds

Owners of new builds will be able to choose either the CGT discount or cost base indexation (with the 30% minimum tax still applicable). New builds include dwellings constructed on vacant land, or where existing properties are demolished and replaced with a greater number of dwellings. Knock down rebuilds or substantial renovations are not considered new builds and therefore will not be eligible. A new build cannot have been previously sold, unless first owned by the builder and not occupied for more than 12 months.

Exemptions

Income support payment recipients (including Age Pension and JobSeeker payment recipients) will be exempt from the 30% minimum tax if they receive payment in the financial year in which they realise the capital gain.

A minimum tax rate of 30% is proposed to be introduced on discretionary trusts from 1 July 2028.

The current Australian taxation laws

Currently, under Australian taxation laws, discretionary trusts are not considered separate taxable entities. Broadly, it is the beneficiaries of discretionary trusts who are ultimately entitled to receive and retain trust income and are taxed on the net income of the trust (as defined for income tax purposes). The trustee is then, generally, taxed on the balance (if any) of the net income (subject to certain exceptions) that is not distributed. Trustees are also taxed if no beneficiaries are made presently entitled to trust income.

Proposed new measure

Under the new measure, trustees will pay a minimum tax of 30% (unless higher rates apply) on the taxable income of discretionary trusts from 1 July 2028. Beneficiaries (other than corporate beneficiaries) will receive non-refundable credits for any tax payable by the trustee.

Trustees will be required to calculate, report and pay the minimum tax, as well as to notify beneficiaries of their entitlements and associated tax credits. The mechanism for collecting the minimum tax will be subject to consultation, but is expected to be consistent with established collection mechanisms. Trustees that receive franked dividends will be required to use their franking credits to pay the minimum tax.

The minimum tax will not be applicable to:

Negative gearing for residential property will be limited to new builds from 1 July 2027.

Broadly, where net losses arise as a result of deductible expenses associated with income-producing property exceeding the income earned from that property, negative gearing allows for this resulting net loss to be offset against other assessable income of the taxpayer.

Proposed new measures

Under the new measures, negative gearing will be limited to eligible new builds only. This means that investors in new builds will still be able to deduct rental losses against other assessable income, such as their salary. New builds include dwellings constructed on vacant land, or where existing properties are demolished and replaced with a greater number of dwellings.

Knock-down rebuilds or substantial renovations are not considered new builds and therefore will not be eligible for negative gearing.

A new build cannot have been previously sold, unless first owned by the builder and not occupied for more than 12 months.

Proposed application of measures

The measure will apply to individuals, partnerships and most trusts. Widely-held trusts (eg most managed investment trusts) and superannuation funds (including self-managed superannuation funds) will be excluded.

Losses incurred from established residential properties will only be deductible against rental income or capital gains arising from residential properties. Any excess losses will be able to be carried forward and offset against income from residential property in future years.

These changes will apply to any established residential properties acquired from 7:30pm (AEST) on 12 May 2026. Any residential properties acquired prior to this time (including any contracts entered into but not settled) will be grandfathered, and will therefore be exempt from the changes until disposed of. Residential properties acquired between 7:30pm (AEST) on 12 May 2026 and 30 June 2027 may be negatively geared during this period, but not from 1 July 2027.

Exclusions

Properties held in widely-held trusts and superannuation funds will be excluded from these measures, with exemptions for build-to-rent developments and private investors supporting government housing programs.

Changes to negative gearing only apply to residential properties. Commercial property and other asset classes, such as shares, will remain eligible for negative gearing. Exemptions to negative gearing will also be available for private investors who support government housing programs (through the provision of affordable housing).

Currently, all electric vehicles that are not a plug-in hybrid are exempt from FBT.

To ensure the system remains sustainable, Australia will transition to a permanent 25% discount on FBT for certain electric vehicles (EVs).

From 1 April 2029, a permanent 25% discount on FBT will be available for all electric cars valued up to and including the fuel‑efficient luxury car tax (LCT) threshold, implemented through a 15% rate in the FBT statutory formula.

The following transitional arrangements will be adopted:

The existing 20% statutory rate will continue to apply for all other cars, including electric cars costing more than the fuel‑efficient LCT threshold.

Reportable fringe benefits will continue to be determined for eligible electric cars as if a 20% FBT statutory formula rate or cost basis method applied.

The Research and Development (R&D) Tax Incentive will be reformed to make it easier to use, increasing the incentive for new businesses to invest in R&D activities.

From 1 July 2028, the measure proposes to:

The venture capital limited partnership (VCLP) and early stage venture capital limited partnership (ESVCLP) tax incentives will be expanded from 1 July 2027. The eligible venture capital investor program will be closed to new applications from 12 May 2026 7:30pm (AEST).

From 1 July 2027:

The Inclusive Framework agreed to a side-by-side package on 5 January 2026 that included the following 5 key components:

Australian legislation will be amended to implement the side-by-side package from 1 January 2026 to ensure Australia’s global minimum tax rules are consistent with those of other implementing jurisdictions.

Funding will be provided from 2026–27 to strengthen governance requirements, supervision and enforcement in relation to managed investment schemes.

In particular:

The government will also consult publicly on new data collection powers in relation to MISs.

Funding will be provided over 2 years from 2026–27 to streamline regulatory systems and secure access to data. Legislation will also be introduced to improve regulation in the financial sector.

Funding initiatives will be provided to streamline regulator systems and secure access to data. These include: